What Exactly is a Chart of Accounts?

Think of the Chart of Accounts as the organizational map for every financial transaction that flows through your business. It is an ordered list of every account in your general ledger, designed to categorize every penny you earn and spend.

Every entry you record—whether it’s income, expenses, asset purchases, or debt payments—must be assigned to one of the accounts on your Chart of Accounts. This systematic categorization is what makes your financial statements accurate and meaningful.

The Importance of Account Types

Understanding the five core account types is the bedrock of setting up your Chart of Accounts (COA). Why? Because the account type dictates two critical things:

Where the account appears on your financial statements. (Balance Sheet or Profit & Loss Statement).

How transactions affect the account balance (i.e., whether a debit or a credit increases or decreases it).

If you assign the wrong type, your financial reports will be wrong, regardless of how accurately you entered the transaction amount. For instance, if you receive a bank loan and mistakenly categorize it as Income instead of a Liability, your Profit & Loss statement will drastically overstate your profit, leading to incorrect business decisions and potentially higher tax liabilities.

The Five Core Account Types

The accounts you need for any business, regardless of industry or size, are built upon five fundamental account categories.

1. Assets: What your company owns (cash, receivables, equipment). Assets make up the first part of your balance sheet.

2. Liabilities: What your company owes to others (payables, loans, deferred revenue). Liabilities are another section of the balance sheet.

3. Equity: The owner’s stake in the company (owner investment, retained earnings). When you add equity and liabilities together, they equal your assets.

4. Revenue/Income: Money your company earns from operations (sales, service fees). Income is one half of your profit & loss statement.

5. Expenses: Costs your company incurs to generate revenue (rent, salaries, marketing). Expenses are deducted from income to determine your net income.

Step 1: Naming Your Accounts for Clarity

Once you know the types, the next step is assigning names. The best names are meaningful and easy for you and your team to understand. There is no secret, standardized list of names.

Good Naming Principles

Be Specific but Concise: Avoid names that are too long (e.g., “Office Papers, Pencils, and Other Supplies”). A short, descriptive name like “Office Supplies” is better.

Use Standard Terms When Applicable: Some accounts have industry-standard names, and you should use them. For example, “Accounts Receivable” (money owed to you by customers) and “Accounts Payable” (money you owe to vendors).

Align with Real-World Accounts: Your books should mirror reality. If you have separate Checking and Savings accounts, you must create a separate entry for each one.

What to Avoid

Vague or Useless Names: An account called “Stuff I Buy” is not helpful for running a business or filing taxes.

Overly Detailed Accounts: You don’t need a separate expense account for every vendor you pay or for every single item you buy (like “Copy paper used in Xerox Machine”). Generally you can use your accounting system’s tracking features (like vendor or product lists) for that level of detail.

Step 2: Utilizing Subaccounts for Detail and Summarization

A key organizational tool for your Chart of Accounts in QuickBooks is subaccounts. Subaccounts allow you to track more detail while still providing a clear summary on your financial reports.

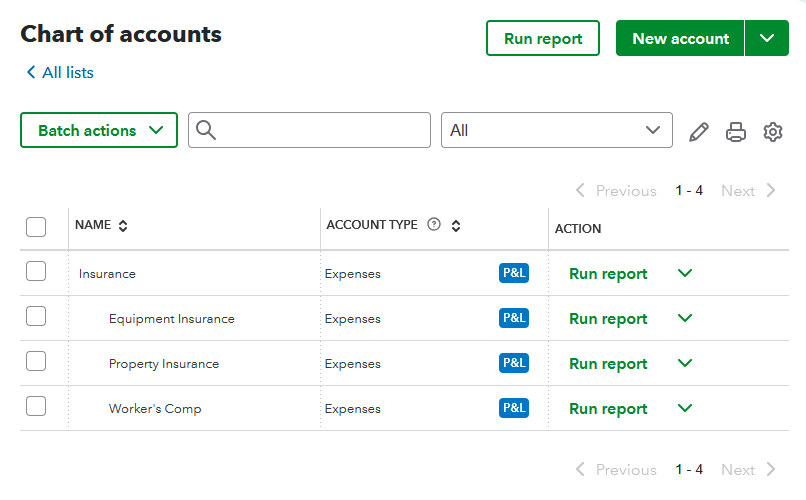

A parent account is the general category (e.g., “Insurance”), and the subaccounts provide the breakdown (e.g., “Equipment Insurance,” “Property Insurance,” “Workers Comp”).

On financial statements, you can often collapse the parent account to see only the total, or expand it to view all the underlying subaccount details. This feature keeps your reports concise for high-level reviews (like sharing with a banker) while providing necessary granularity for internal management.

Step 3: Deciding on Account Numbers

While not strictly necessary for modern bookkeeping software, using account numbers is a classic accounting practice that can still provide organizational benefits.

Standardization: Accountants often use a standardized numbering scheme across different clients, making it easier for them to remember the correct account for a transaction.

Easy Entry: You can quickly enter a transaction using the account number instead of typing out the full name.

Custom Sorting: Account numbers override alphabetical sorting, allowing you to organize your Chart of Accounts and reports in a specific, logical order that you prefer.

If you choose to use account numbers, ensure the numbering scheme is logical and easy to recall.

Final Setup Checklist

Before you begin recording your first transaction, ensure your Chart of Accounts meets these criteria:

- All Five Core Account Types are represented.

- You have sufficient detail to file your tax return easily (e.g., separate accounts for travel, meals, fuel).

- Account names are clear, concise, and meaningful to everyone in the business.

- You have a separate account for every real-world bank account (checking, savings, etc.).

- You use subaccounts to provide detail for internal management without making the main reports overly long.

- You have worked with your accountant to confirm the accounts they will need for year-end reviews and tax adjustments.

Next Step

Now that you understand how to set up your Chart of Accounts correctly, it’s time to put this knowledge into practice. We offer comprehensive QuickBooks training that covers Chart of Accounts setup, transaction recording, and financial reporting—everything you need to build a solid financial foundation for your business.